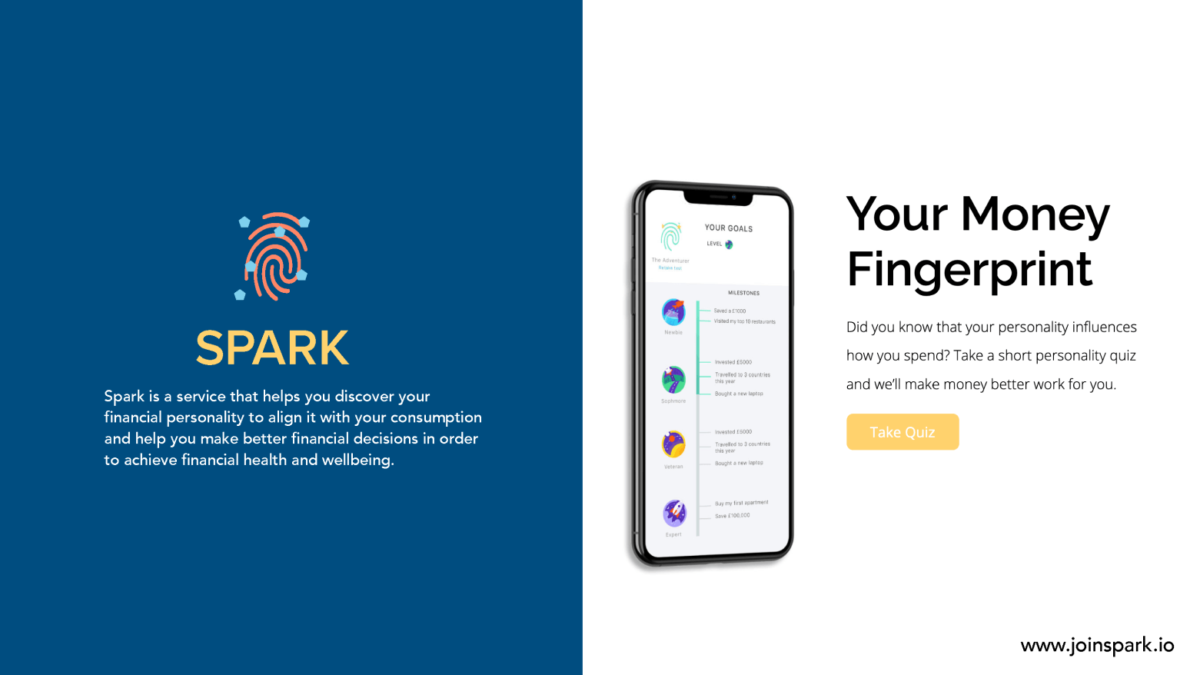

Spark is a service that helps you discover your financial personality to align it with your consumption. It helps you make better financial decisions and achieve financial health and wellbeing.

What is the problem?

We know that people do not always act rationally or in alignment with their intentions, which from a financial perspective often means that money is not used in the ways that bring people the most happiness. This could be because it is either spent too much at times when frugality would bring more happiness or because it is spent on things that are not the optimal way to exchange money for personal value.

Within this context, we can look to the world of financial institutions and argue that the services in place to serve people financially are set up to profit from people’s bad decisions rather than to help people achieve more wellbeing. For young people just graduating college and entering their first jobs, there is a sense of anxiety that they do not have the necessary control over their money and that the way they interact with services often feels like a ‘one-size-fits-all’.Ultimately, they feel the solutions provided don’t fit their lives. Moreover, people’s financial behaviour changes according to their personality, meaning that you will spend and save money in different ways, and that you will take happiness from how you’ve spent your money in different ways depending on your personality.

There is a mismatch between banking services’ blanket approach to supporting people financially and the reality of how people interact with and value money. It’s in this environment that young people are leaving education with low financial literacy, low savings and new financial responsibilities and expectations. This not only leads to anxiety around financial decision-making, but also to ineffective relationships with money that can perpetuate and have serious implications on people’s lives.

How ‘Spark’ responds

Spark responds to these issues by integrating the attributes of more personalised lifestyle services with typically rigid financial tools. This means that not only does the service understands its users and customises the advice it gives accordingly but it is able to tune the entire service right down to the financial dashboards. In this way, the objective of the service is to help align how someone uses their money with their personality type. In doing so, it builds clarity and a sense of control that can improve people’s long term financial health and wellbeing.

Personality Test:

When they start the service, the first thing people do is complete a quiz about their personality, which provides them with a match, showing them how people with their personality typically like to spend, save or invest. Money does not equal happiness, but when people spend their money according to their personality, it can lead to more happiness. This personality test is the first step to creating a bespoke service for each user.

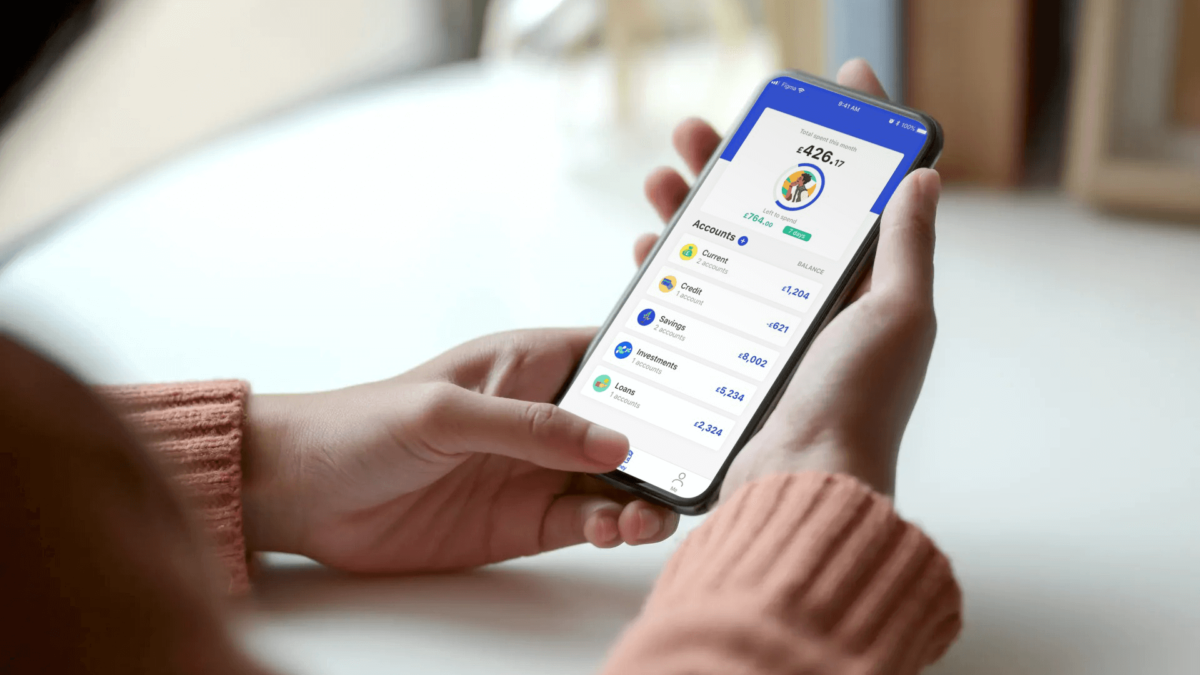

Mirror:

Through open banking, people connect their different accounts so that Spark can analyse and then reflect back to people how they spend their money. These categorisations and visualisations can give a fresh perspective, which can help people understand where their money is going and how much they’re really saving. This alone may help people find a new level of control and illuminate opportunities for new habits that will make them happier.

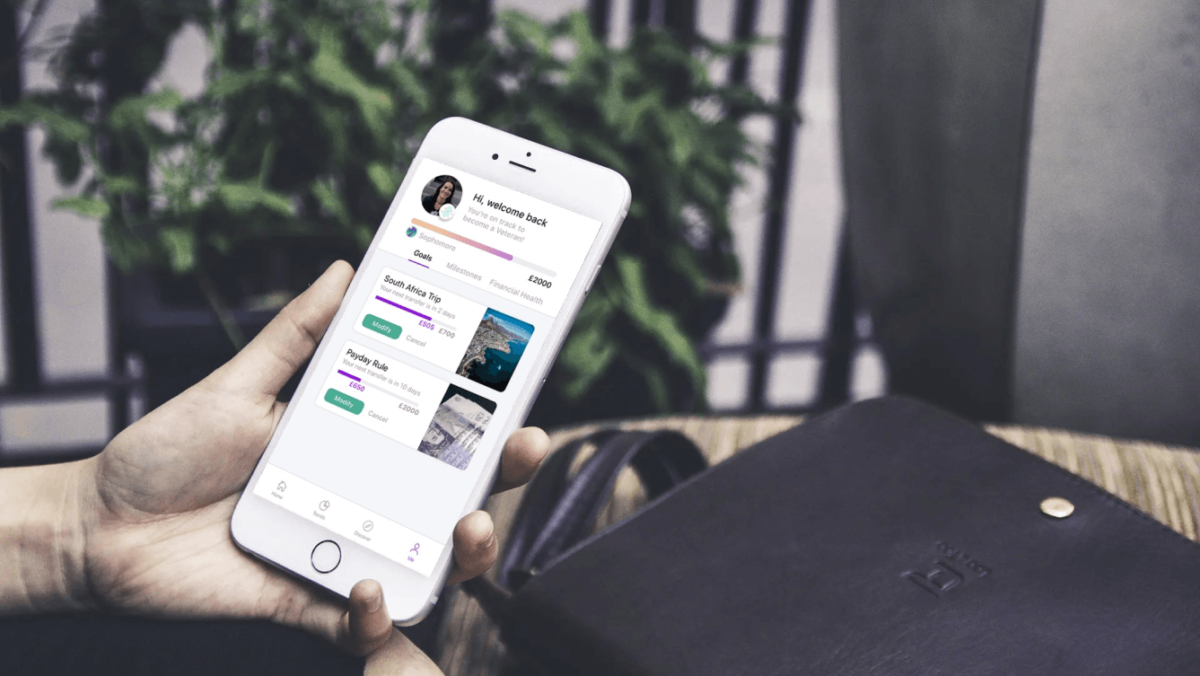

Goals and Advice:

Spark combines its understanding of people’s personality and their spending behaviour with specific financial and life goals so that it can provide the most meaningful advice possible. It’s able to show people a path forward of what can be achieved if they take Spark’s financial advice.

Access:

Finally, Spark gives each user a financial health score based on their financial behaviour . This score is connected to how well they are progressing toward a goal or how much they are improving. A high score means a user has access to other Spark accredited financial services like a low cost loan or or a better credit card.

What we

learnt

We demonstrated a low fidelity prototype of Spark to our users and their response was very positive, generally demonstrating a high desirability and a promising area of opportunity for using these approaches to improve people’s control over their finances. The proposition also sheds light on some interesting questions that emerge as services move into these new spaces.

It’s clear that there is a relationship between people’s personalities and their financial habits. When this relationship is incorporated into services, it can offer people more control and potentially greater happiness for the same amounts of money. However, while tailoring financial services to people’s personalities might be good for some people, it’s not clear how vulnerable these systems may be to bias (against particular personalities) or what it means when a user shifts between genuinely changing their character or behaviour, playing the game just to do better, or simply cheating the system. Below we explore the overall topics.

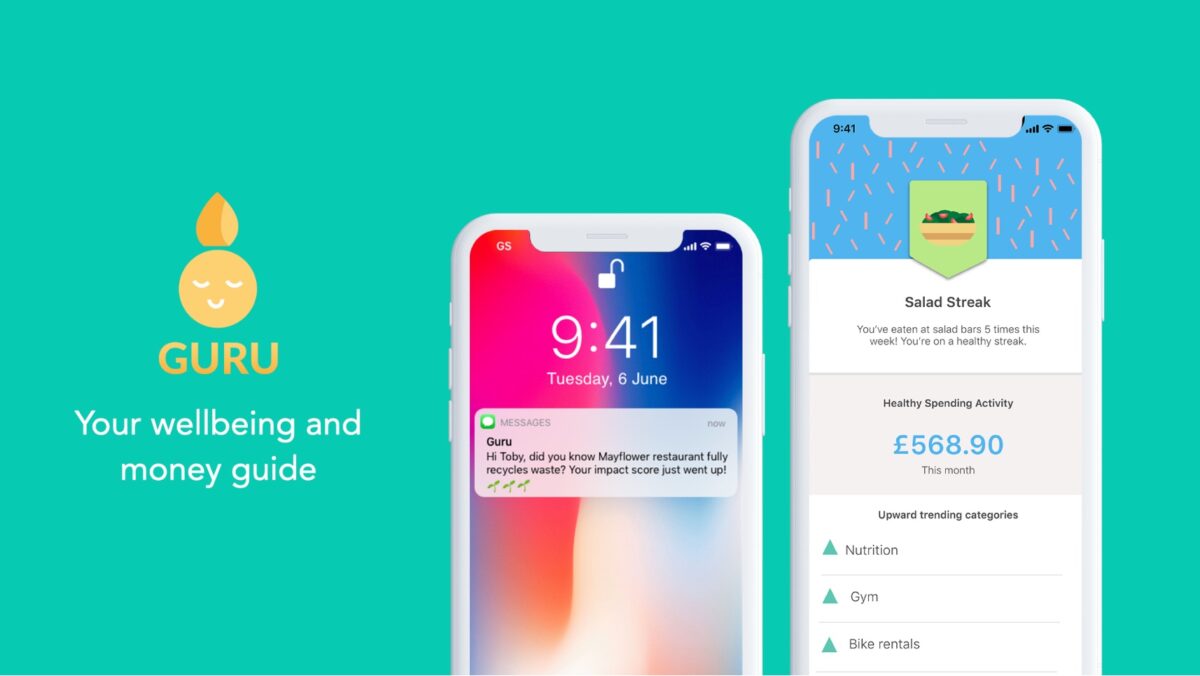

Engagement

Through the research, we realised that there was a lot of connection between people’s anxiety and stress and their financial health, but that money management was seen as boring for the target users. The perception was that these financial considerations were something for later in life so the challenge in the service is about how to help people engage in a productive but seemingly ‘boring’ process.

Users found Spark to be valuable because it responded to this problem by making it fun and engaging. Firstly, by stating that there is financial gain to be had from using the service, then by using an engaging and illuminating quiz and finally, by making the service about almost everything else except money and visualising money in relatable terms like the number of activities they could do with it. It’s through these mechanisms that people were able to enjoy the concept. We found that even by simply visualising people’s money differently, behaviour could be changed, and this could ultimately lead to increased wellbeing.

Avoiding addictiveness

We found that there was some concern among users that a service like this could become too addictive. The gamified elements of the service make it fun, which in combination with the importance of money in people’s lives and how often they interact with it, it seems that it could become a fertile ground to cause addiction, which would ultimately have a negative impact on people’s anxiety levels. In response, Spark could attempt to recognise addictive behaviour and move certain activities into the background to prevent the user from over-interacting with the service in unhealthy ways.

Avoiding biases

An emerging issue within the spark concept is around how a service like this can base its offerings on someone’s personality in order to tailor the service, without also risking excluding people from financial services because they might have personality traits that are less ‘financially attractive’.

When considering access to credit, people can adapt how they look in the app and play the system to get the best financial opportunity. However, there is also a risk that people with less common personality traits may not get access to a financial opportunity because their profile is poorly understood and therefore represents a risk. How can financial services adjust to people’s personalities without essentially discriminating against people based on their personality?

Playing, Cheating or Changing

We also see an emerging issue regarding how people might adapt to financial gain. If we envisage a scenario where people are able to convince a service that their personality is more financially attractive, then there is a lot of evidence to suggest that people will do so. If we build on this scenario, proposing that in the future someone’s personality will be more intricately understood by the service through more sophisticated data and analysis —at what point does it become impossible for the user to game the service and to what extend would users adjust themselves and their lives and the appearance of their personality to be seen as more ‘financially attractive’? Could the overlapping of personality and finance, in more sophisticated ways, lead to the emergence of characteristics that cost people more money, essentially ‘expensive personality traits’?

The proposition is premised on the idea that by offering people information about their personality, their behaviour and the financial system, they can be more in control of their finances and their financial wellbeing. Users are essentially encouraged to play a game with their personality and their behaviour in order to improve their financial wellbeing. At what point does playing the game mean sacrificing too much for the sake of financial wellbeing ?

Jump to:

Service visions

Guru

Our new direction of exploration

If this proposition is progressed, the strategic question of relevance to our investigations is more along the lines of:

As the world of financial wellbeing overlaps with sophisticated personality assessment, how can we find a balance that encourages an appropriate level of gaming one’s life for financial wellbeing, without damaging people’s freedom to be who they want to be or discriminating against people based on their personalities?

Nafeesa Jafferjee

Related to ‘Spark’

Scenarios

Emotional money

AI could advance to levels that would allow sophisticated understanding of people’s emotions. If that information is coupled with financial behaviours or organisational objectives it could transform how value is assigned to our services and our experiences.